| Read in browser | ||||||||||||||

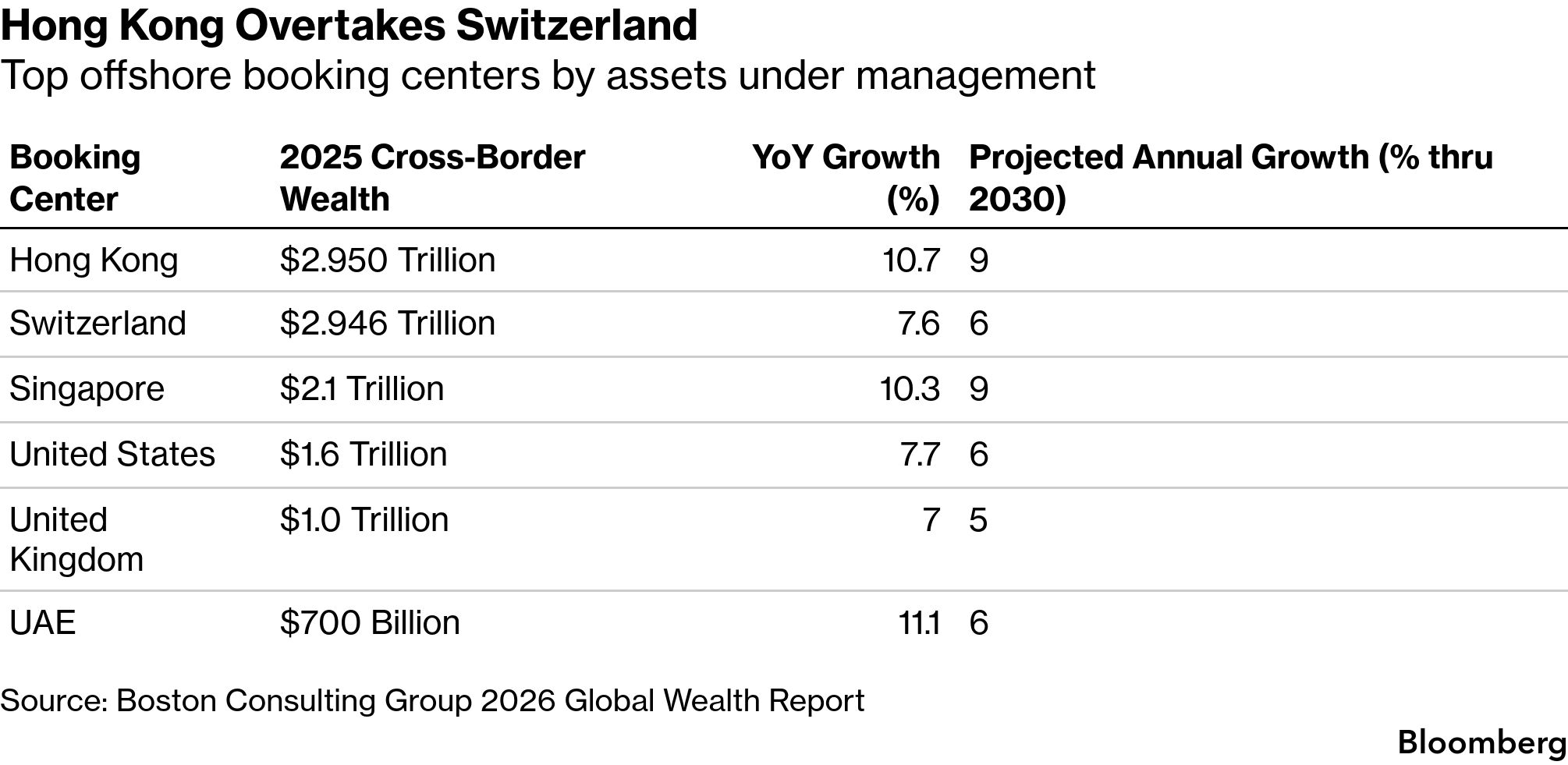

Wall Street is listening. Blackstone and Guggenheim Investments are among big firms slashing their software exposure in recent collateralized loan obligation deals. The maneuver follows a sharp selloff in the debt of software firms which borrowed heavily in the leveraged loan market to fund a wave of buyouts by private equity funds. Guggenheim is even said to have recently priced a roughly $560 million CLO it marketed as software-free. Fears that artificial intelligence may render software makers obsolete has been driving equity investors to sell, prompting embattled companies to release earnings early to shore up confidence just as high-profile financiers seek to defend the sector. It’s part of the broader economic earthquake triggered by new AI models, a disruption with no discernible end in sight. Software borrowers now account for about 13.2% of the loans in US CLO deals, down from almost 14% at the end of last year. But while software scrutiny has intensified, some CLO managers recently — and successfully — came to market with software-heavy portfolios, showing there’s not a blanket refusal on the sector. But there’s a hitch. Some CLO managers use inconsistent industry classifications to identify borrowers — categories the ratings agencies use to gauge portfolio diversification. What You Need to Know TodayLest anyone think the questions swirling around the private credit market have gone away, news from Switzerland will disabuse you. It only took one whale who wanted out to spur a Vista Equity Partners private credit fund to enforce its 5% limit on withdrawals last month. A Switzerland-based pension fund is said to have sought to redeem all of its shares from Vista Credit Strategic Lending in the first quarter. The withdrawal request from a single institution, rather than legions of retail investors, puts a different spin on the redemption pressure that’s engulfed the $1.8 trillion private credit market as concerns mount over the aforementioned software loans. Hong Kong has narrowly overtaken Switzerland to become the world’s largest cross-border wealth hub, driven by an influx of mainland Chinese capital and a resurgent local equity market.  The shift comes as global private fortunes expand at their fastest clip since 2021, defying the US trade war and macroeconomic instability to reach a total of $333 trillion. While Hong Kong and Singapore form an expanding ecosystem serving Asian capital, Switzerland, the US and the UK remain primary conduits for European, Middle Eastern and Latin American wealth. Hong Kong, hoping to reclaim its allure after years of pandemic restrictions and political upheaval, is aggressively pitching its low taxes, deep talent pool and booming capital markets to the global elite. The strategy is working: geopolitical tensions, including the US-Israel war with Iran, are prompting the ultra-wealthy to diversify into Asia. A post-IPO merger between SpaceX and Tesla is inevitable and only a question of timing, according to early SpaceX investor Peter Diamandis. The reason? Power. Elon Musk’s power, that is. Diamandis told Bloomberg Television the combination makes sense as it would give the South Africa native the super voting rights he has at SpaceX — where he had 85.1% control before the filing for an initial public offering — but lacks at publicly held Tesla. Merging the companies would give Musk “the ability to operate across all of this infrastructure,” he said, including a fleet of Cybercab robotaxis and Tesla vehicles with compute and power capability, creating “a global infrastructure on the ground and in space.” Hours after BP ousted him, former BP Chairman Albert Manifold said he had been fired without warning or explanation and will challenge the company’s version of events. The very public conflict deepens the turmoil around the UK oil major’s latest leadership change, and larger questions about the company’s processes and future. BP, which citied unspecified serious concerns related to Manifold’s “governance standards, oversight and conduct” in its statement on Tuesday, has seen three leaders in as many years.  Albert Manifold Photographer: Chris Ratcliffe/Bloomberg Wall Street banks are predicting another banner quarter for their trading desks. Bank of America said it expects second-quarter revenue from sales and trading to increase about 15% from a year ago, and JPMorgan said markets revenue at the bank could rise 11%, which would make it the second-best quarter ever for that business. Trading gains already helped fuel a record haul for the biggest US banks in the first three months of 2026, with stock trading in particular benefiting from a wave of volatility generated by the Iran war and concern about disruptions from AI and private credit. Spring Sale: Save 60% on your first year Get the numbers behind the narratives. Enjoy unlimited access to Bloomberg.com and the Bloomberg app, plus market tools, expert analysis, live updates and more. Offer ends soon. Unlock 60% offWhat You’ll Need to Know TomorrowFor Your CommuteBloomberg Tech returns to San Francisco on June 3-4 as Emily Chang and Tom Giles convene some of the CEOs, investors and innovators shaping the future. Drawing on Bloomberg’s global newsroom and Terminal data, we’ll explore the capital, connectivity and ideas driving the industry forward. Register here. More from BloombergEnjoying Evening Briefing Americas? Get more news and analysis with our regional editions for Asia and Europe. Check out these newsletters, too:

Explore all newsletters at Bloomberg.com. We’re improving your newsletter experience and we’d love your feedback. If something looks off, help us fine-tune your experience by reporting it here. Follow Us You received this message because you are subscribed to Bloomberg’s Evening Briefing Americas newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.

|